Tax incentives for build-to-rent developments

On 28 April 2023, the Australian Government announced it would provide incentives to increase the supply of housing by:

- Reducing the withholding tax rate for eligible fund payments from managed investment trusts (MIT) attributable to residential build-to-rent projects from 30% to 15%. This measure will apply from 1 July 2024 for income attributable to newly built build-to-rent projects.

- Increasing the capital works tax deduction depreciation rate for eligible new build-to-rent projects from 2.5% to 4% per year. This measure will apply to projects where construction commences after the Budget (9 May 2023) and will shorten the period that construction costs of eligible buildings are depreciated from 40 to 25 years.

These incentives only apply to build-to-rent projects comprising 50 or more apartments or dwellings made available for rent to the general public. The dwellings must be retained under single ownership for at least ten years. In addition, landlords must offer a lease term of at least three years for each dwelling.

Similar posts you may like

- Tom Peters had it right, excellence isn’t an accident. It’s a decision.

I revisited In Search of Excellence recently. Written in 1982, but the core message still cuts through: Stop comparing yourself to the average. Look at Read more

- Overturning the ‘backpacker tax’

British working holiday visa holders in Australia have been forced to pay a flat rate tax higher than Australian residents without the tax-free Read more

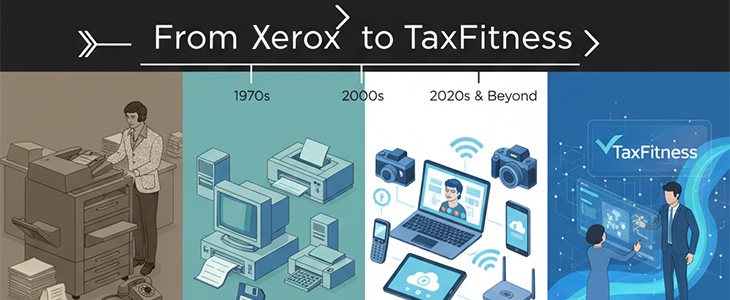

- From Xerox to TaxFitness, the power of benchmarking

In the early 1980s, Robert C. Camp at Xerox faced a hard truth — Japanese competitors were producing higher-quality products at lower cost. Instead of guessing, Read more

- Want to be a top 20% accounting firm? Here’s the blueprint

The highest-performing accounting practices aren’t just profitable—they dominate the industry with smarter pricing, stronger client retention, and efficient operations. Are you hitting these benchmarks? Read more

"You’d be stupid not to try to cut your tax bill and those that don’t are stupid in business"

- Bono: U2