The 2026–27 Federal Budget introduced significant changes affecting individuals, businesses, investors and discretionary trusts. TaxFitness has translated these changes into eight practical tax-planning strategies: TS 203 – Review discretionary trusts before the proposed 30% minimum tax TS 272 – Access refundable losses for eligible start-ups TS 34 – Obtain asset valuations at 1 July 2027…

Most accountants don’t have a benchmarking problem. They have a systems problem. “Benchmarking is too complex” is the excuse. The reality is simpler: if it takes hours to produce a benchmarking report, you’re not doing benchmarking, you’re doing manual labour. Spreadsheets, rework, inconsistent data, and starting from zero every time. That’s not insight. That’s inefficiency.…

Carla O’Dell didn’t just promote benchmarking, she scaled it globally. As CEO of the American Productivity & Quality Center (APQC), she transformed benchmarking from an internal exercise into a structured, cross-industry knowledge system. Before APQC, benchmarking was internal, isolated and tactical. Under her leadership, it became cross-industry, data-driven and institutional. Her key insight was simple: data has…

Scan 50 accounting firm websites. You’ll see: Business advisory. Strategic advice. Helping you grow. Inside the firm? Still compliance. Here’s the truth. Most firms claiming advisory: Have no system No defined process No structured deliverables No modelling tools No pricing framework No supporting software It lives in the partner’s head. If you can’t: Run it…

When salary return numbers drop, the obvious question is: “Where does that revenue get replaced?” For some firms, it won’t be. If your firm’s value is tied to checking receipts and lodging forms, there’s no natural upgrade path. The work just disappears. But for firms that understand advisory, the shift is straightforward. The $1,000 standard…

Most wreckers chase volume. More cars. Bigger yard. Longer days. Top-20% wreckers focus on profit per vehicle. Here’s what the data shows. Top-20% Auto Wreckers Revenue: $1.1m – $1.4m COGS: 30% – 35% Wages: 20% – 30% Net profit: 15% – 20% Parts sales: 75% – 85% of revenue Inventory turnover: 2.5x – 4x Quote conversion: 50% – 65% Same industry. Same cars.…

From 1 July 2026, the ATO is introducing a $1,000 standard work-related deduction. If a client’s deductions are $1,000 or less, they can claim it without receipts. If they’re over $1,000, nothing changes. Records still matter. Advice still matters. This change doesn’t make accountants redundant. It exposes where time has been wasted. Chasing receipts for basic deductions…

Too many accountants ask me the same question: “How do we actually turn tax planning and advisory into real revenue — not just nicer reports?” Here’s the honest answer. Software alone doesn’t do it. Neither does a one-off webinar or a template download. What works is guided execution, applying the work with real clients, refining it,…

Most accountants underestimate one of the easiest wins sitting right in front of them: Occupation-specific tax advice. Generic deduction lists don’t cut it anymore. Clients want clarity, not guesswork — and they want to know you understand their world, not just “tax rules”. That’s why we built the TaxFitness Occupation Deductions Database — now covering…

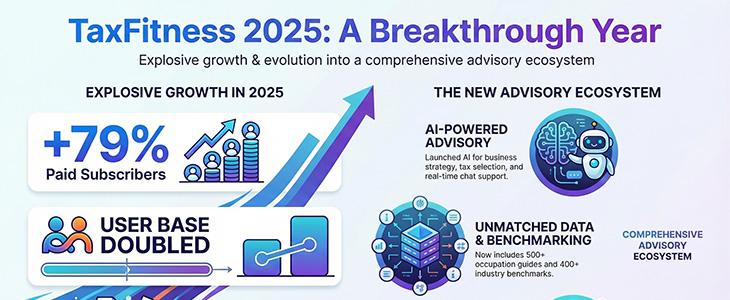

As we close out 2025, I wanted to share where TaxFitness has landed and, more importantly, where we’re heading. This year has been the biggest step forward we’ve taken since the platform launched. Not just more users. Not just more features. A genuine shift in how accountants deliver advice. 𝗛𝗲𝗿𝗲’𝘀 𝘁𝗵𝗲 𝘀𝗻𝗮𝗽𝘀𝗵𝗼𝘁: Paid subscribers up…

Similar posts you may like

- Tax Planning Strategy 178 – Auto Reversionary Pension

A reversionary pension is a pension that is paid to a member and on the death of the member continues to be paid to Read more

- Federal Income Tax Introduced (1915)

A federal government income tax was introduced in 1915, in addition to existing state income taxes, to finance involvement in the First World War. Read more

- Employee share plan trust

Employee share schemes (ESS) give employees shares in the company they work for, or the opportunity to buy shares in the company. Employees generally Read more

- Most firms say they do advisory. Most don’t

Scan 50 accounting firm websites. You’ll see: Business advisory. Strategic advice. Helping you grow. Inside the firm? Still compliance. Here’s the truth. Most firms Read more

"You’d be stupid not to try to cut your tax bill and those that don’t are stupid in business"

- Bono: U2