Part IVA – the ATO’s ultimate weapon against tax schemes

Not all tax planning is created equal. The General Anti-Avoidance Rules (GAAR) in Part IVA of the Income Tax Assessment Act 1936 give the ATO sweeping powers to unwind transactions it sees as tax avoidance – and impose penalties of up to 50% of the tax payable.

Key questions Part IVA asks:

- Was there a scheme?

- Was a tax benefit obtained (e.g., extra deductions, avoided income)?

- Was the dominant purpose to gain that tax benefit?

- What’s the commercial substance of the transaction?

If the ATO determines a taxpayer’s primary purpose was tax avoidance – even if the transaction is also commercially sensible – Part IVA can apply. It doesn’t matter if the scheme is technically “legal”. If it lacks substance, you’re exposed.

At TaxFitness, we show accountants how to help clients minimise tax legally and ethically – with:

- 600+ proven, compliant tax strategies

- Clear documentation to support commercial purpose

- Avoidance of red flags that could trigger Part IVA

Smart tax planning is about more than saving tax. It’s about doing it right. Chapter 15 of our Benchmarking Manual is titled: Keep Everything Legal – and Part IVA is front and centre. Learn more by booking a demo here.

Similar posts you may like

- Import newsletter content into your Mailchimp account in seconds!

If you have a subscription service such as TaxFitness that allows you to use newsletter content to send to your own clients, there is Read more

- First State Income Tax (1880)

Tasmania was the first state to introduce an income tax in 1880 to raise revenue due to a fiscal crisis. The tax took Read more

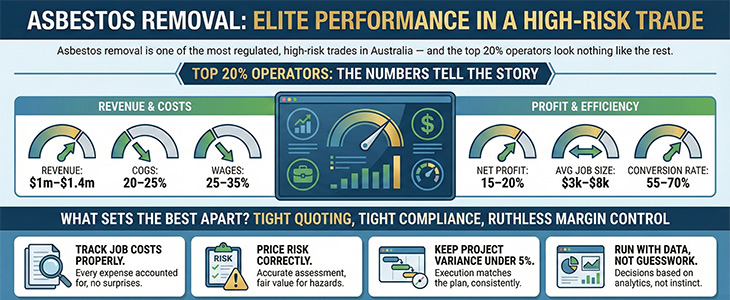

- Asbestos removal is one of the most regulated, high-risk trades in Australia – and the top 20% operators look nothing like the rest

Asbestos removal is one of the most regulated, high-risk trades in Australia — and the top 20% operators look nothing like the rest. Their Read more

- 1710 – A Tax on Playing Cards

A playing card is a piece of specially prepared heavy paper, plastic-coated paper, cotton-paper blend, or thin plastic, marked with distinguishing motifs and used Read more

"You’d be stupid not to try to cut your tax bill and those that don’t are stupid in business"

- Bono: U2